When you fill a prescription, you might not realize there's more than one version of the same drug on the shelf. Some are branded. Some are regular generics. And then there are authorized generics-a quiet but powerful option that can save you and your insurer money without changing how the drug works. But here’s the catch: not all insurance plans treat them the same. Understanding how authorized generics fit into formulary placement can make a real difference in what you pay and what you get.

What Exactly Is an Authorized Generic?

An authorized generic isn’t just another generic drug. It’s made by the same company that produces the brand-name version, using the exact same formula, ingredients, and manufacturing process. The only difference? It doesn’t carry the brand name on the label. Think of it like buying a store-brand cereal that’s made in the same factory as the name-brand version. You’re getting identical quality, just without the marketing.

The U.S. Food and Drug Administration (FDA) defines authorized generics as drugs approved under the original New Drug Application (NDA). That means they skip the usual generic approval path (the ANDA process) and don’t need to prove bioequivalence again. They’re identical from the first pill to the last. As of 2023, the FDA listed 147 authorized generics, including popular drugs like Protonix, Ocella, and Yasmin.

Why Insurance Companies Care About Them

For insurers, authorized generics are a sweet spot. They offer the same clinical results as the brand-name drug but at generic prices-usually 15% to 25% cheaper. That’s huge when you’re managing millions of prescriptions across thousands of patients. Unlike traditional generics, which can take months to launch due to patent disputes or exclusivity periods, authorized generics can hit the market the day the brand patent expires. That means insurers can start saving immediately.

According to a 2022 Health Affairs study of over 1,200 Medicare Part D plans, 87% placed authorized generics in the same tier as regular generics (usually Tier 2). Only 12% treated them like brand-name drugs. Plans that had clear policies for authorized generics saw 7.3% lower per-member-per-month drug costs. That’s not just a small win-it’s a major cost-saving lever.

How They Compare to Regular Generics

It’s easy to confuse authorized generics with regular generics. But here’s the key difference:

- Regular generics are made by different companies, must prove they work the same way (bioequivalence), and go through the ANDA process. They can take years to enter the market after a brand patent expires.

- Authorized generics are made by the brand company itself, use the same NDA, and launch right away. No extra testing needed.

Because of this, authorized generics avoid the “first generic” exclusivity period that delays competition. That’s why they often appear before any other generic version hits the shelves. For patients on medications with narrow therapeutic windows-like blood thinners or thyroid hormones-this matters. Switching to a regular generic might trigger a reaction or require dose adjustments. Authorized generics eliminate that risk entirely.

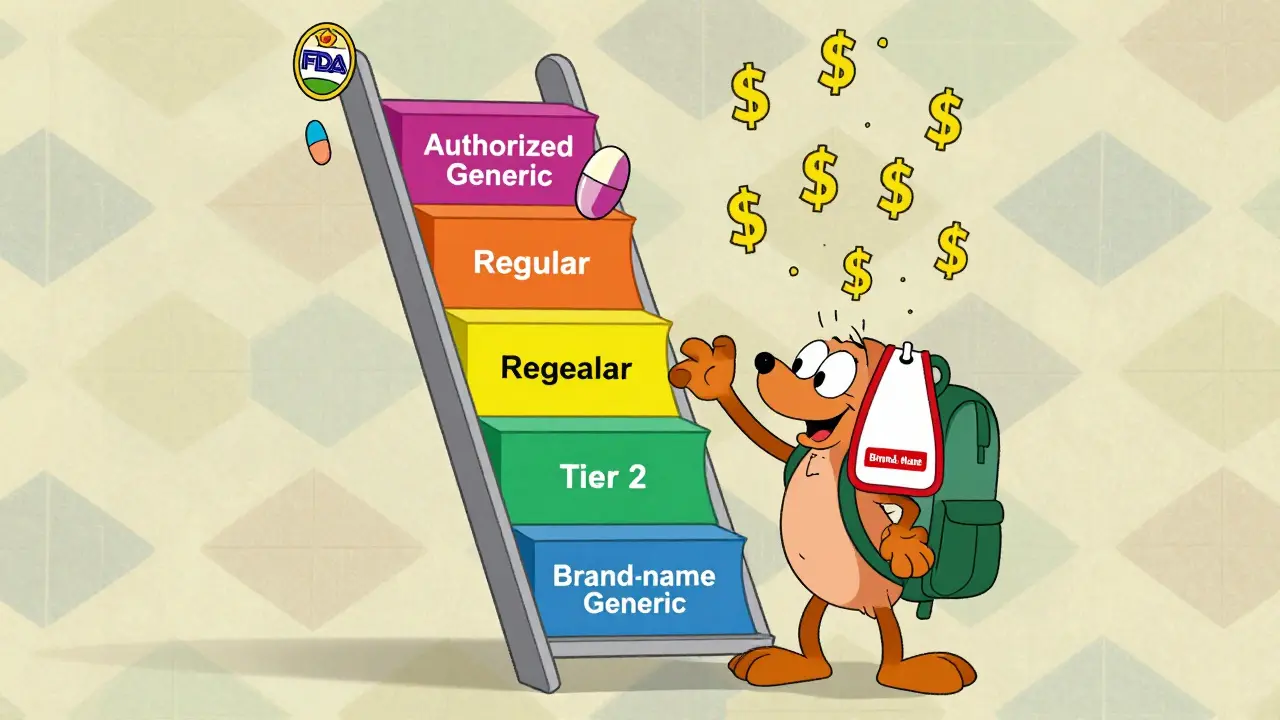

Formulary Placement: Where They Fit

Insurance formularies rank drugs into tiers based on cost and clinical value. Tier 1 is cheapest (usually generics), Tier 3 or 4 is most expensive (brands). Authorized generics almost always land in Tier 2, same as regular generics. That means lower copays-often $10 to $15 instead of $50 or more for the brand.

But here’s where things get messy: not all pharmacies or systems recognize them right away. Authorized generics aren’t listed in the FDA’s Orange Book (which tracks approved generics). Instead, they’re tracked separately. If your pharmacy’s system doesn’t have the right NDC code, it might flag the drug as “brand” and charge you the higher price. That’s why some patients report being denied coverage at first-until the pharmacist manually overrides it.

According to Express Scripts’ 2023 report, 89% of authorized generic claims were approved on the first try. That’s close to the 92% approval rate for regular generics. But brand-name drugs? Only 76% got approved immediately. So while authorized generics aren’t perfect, they’re far more reliable than the brand.

Real Patient Stories

One Reddit user, u/MedicationWarrior, shared: “My insurance denied Synthroid (brand) because it was too expensive. I asked if they had the authorized generic. They did. Same pill, $10 copay. I’ve been stable for two years now.”

Another patient, who had severe allergies to dye in brand-name medications, switched to an authorized generic of a heart drug and avoided a hospitalization. “The ingredients were identical,” they wrote. “My doctor didn’t even need to change anything.”

But not everyone has smooth sailing. A 2022 GoodRx survey found 34% of patients were confused when their pharmacy switched them to an authorized generic without telling them. Some even thought they were getting a lower-quality drug. Clear communication from pharmacists and insurers is still lacking.

Who Makes Them and Why It Matters

Three companies dominate the authorized generic market: Greenstone (a Pfizer subsidiary), Prasco, and Patriot Pharmaceuticals. Together, they produce 63% of all authorized generics. That concentration means manufacturers have control over when these versions appear-and sometimes, they delay them to protect brand sales.

That’s led to criticism. Dr. Peter Bach from Memorial Sloan Kettering found that in 22% of cases, authorized generics were used to block true generic competition. If the brand company releases its own generic version right away, other companies can’t enter the market. That keeps prices high longer than they should be.

Still, for patients and insurers, the immediate benefit often outweighs the long-term concern. If you need the drug now, an authorized generic is usually your best bet.

What’s Changing in 2026?

Since 2022, things have shifted fast. The Inflation Reduction Act pushed CMS to encourage more authorized generic use in Medicare Part D. By 2025, CMS expects coverage to rise 15-20%. Major pharmacy benefit managers (PBMs) are acting too. OptumRx launched an “Authorized Generic First” policy for 47 high-cost drugs in January 2023. Express Scripts added special flags in their system to make sure these drugs get the right tier.

Even employers are getting involved. The Kaiser Family Foundation’s 2023 survey found 68% of large employers plan to treat authorized generics differently than regular generics in 2024 plans-often giving them even lower copays. That’s a sign they’re being seen not just as cost-savers, but as smart clinical choices.

What You Need to Do

If you’re on a brand-name drug, ask your pharmacist: “Is there an authorized generic version?” If there is, it’s likely cheaper and just as effective. Don’t assume your insurance will automatically cover it-sometimes you need to request it.

Check your plan’s formulary. Look for the drug name without the brand. If you see “[Drug Name] (authorized generic),” it’s probably in Tier 2. If you’re denied, ask for a manual override. Many pharmacists can do this if they know the NDC code.

Keep a list of your medications and ask your doctor to note: “No substitution unless authorized generic.” That’s especially important if you have allergies or sensitive conditions.

Bottom Line

Authorized generics are one of the most underused tools in lowering drug costs without sacrificing safety. They’re not a trick. They’re not a loophole. They’re the exact same drug, just sold without the brand name. And if your insurance plan covers them properly, they can cut your out-of-pocket costs by half.

The system isn’t perfect. There are gaps in recognition, confusion in communication, and strategic delays by manufacturers. But for now, they’re your best bet for getting brand-quality medicine at generic prices. Know what to ask for. Push back when you’re charged more. And remember: you’re not getting a cheaper drug-you’re getting the same drug, without the markup.

Are authorized generics the same as brand-name drugs?

Yes. Authorized generics contain the exact same active and inactive ingredients, dosage, strength, and route of administration as the brand-name drug. They’re made in the same facility, using the same process, and are approved under the original New Drug Application (NDA). The only difference is the label-no brand name, no marketing.

Why do some insurance plans deny coverage for authorized generics?

Sometimes it’s a technical issue. Authorized generics aren’t listed in the FDA’s Orange Book, so pharmacy systems may not recognize them as generics. If the pharmacy’s database doesn’t have the correct NDC code, the system might treat the drug as brand-name and charge a higher copay. This can be fixed by manually updating the system or requesting a formulary exception.

Can I ask my doctor to prescribe an authorized generic?

Absolutely. You can ask your doctor to write the prescription using the generic name and note “substitution allowed” or “authorized generic preferred.” Many doctors are unaware of the distinction, so bringing up the option helps. If your drug has an authorized version, it’s often the best choice for cost and safety.

Do authorized generics have the same side effects as brand-name drugs?

Yes. Because they’re chemically identical, side effects are the same. In fact, patients with allergies to dyes or fillers in brand-name drugs often switch to authorized generics successfully because the inactive ingredients match exactly. This is especially important for drugs like Synthroid, where even tiny differences can affect thyroid levels.

How do I find out if my drug has an authorized generic?

Check the FDA’s official list of authorized generics at fda.gov/drugs/development-approval-process/authorized-generics. You can also ask your pharmacist or use tools like GoodRx or Drugs.com, which now flag authorized generics. If your drug is listed there, it’s worth asking your insurer to cover it.

Chris Beckman

so authorized generics are just brand drugs with the logo scraped off? lol. i always thought generics were made by some sketchy factory in india. turns out the same company that made my $200 pill is now selling it for $15 under a different label. capitalism is wild.

Richard Elric5111

It is imperative to recognize that the ontological equivalence of authorized generics vis-à-vis their branded counterparts is not merely a pharmacological assertion but an epistemological imperative grounded in regulatory fidelity. The FDA’s adherence to the New Drug Application paradigm ensures ontological continuity, thereby obviating the necessity for redundant bioequivalence protocols. This is not a loophole-it is a logical extension of regulatory parsimony.

Betsy Silverman

I’ve been using the authorized generic for my thyroid med for years. My pharmacist didn’t even tell me until I asked. Now I save $40/month and my labs are perfect. It’s weird how something so simple gets buried under all the marketing noise.

Ivan Viktor

So let me get this straight. The same company that charges you $500 for a pill makes a cheaper version of the exact same pill… and then you’re supposed to be grateful they didn’t raise the price? Yeah, I’ll pass.

Zacharia Reda

Wait, so if the brand company makes the authorized generic, aren’t they just playing both sides? They get to block other generics by releasing their own version first? That’s not saving money-that’s just moving the deck chairs on the Titanic.

Jeff Card

I had a friend who switched to an authorized generic for her blood pressure med and had a bad reaction. Turned out the inactive ingredients were different-same active compound, but different dye. Her doctor didn’t know either. So yeah, ‘identical’ doesn’t always mean ‘safe for everyone.’ Always check the label.

Matt Alexander

If your drug has an authorized generic, just ask for it. No magic. No trick. Same pill, cheaper price. Pharmacies know how to do it. Just say the words: ‘I want the authorized generic.’ It’s that simple.

Gretchen Rivas

Ask your pharmacist. Always. I didn’t know this existed until last year. Now I save $120/month. Small change for some, life-changing for others.

Stephen Vassilev

Let’s not pretend this is altruistic. The FDA’s ‘authorized generic’ loophole is a corporate maneuver engineered by Pfizer, Prasco, and Patriot to monopolize post-patent markets under the guise of consumer benefit. This is not innovation-it’s regulatory capture. The fact that these drugs aren’t listed in the Orange Book? That’s not an oversight. That’s the trap.

Mike Dubes

just found out my insulin has an authorized generic. switched last month. same results, $30 less. i had no idea. my dr didn’t mention it. my pharmacist had to explain it. why is this not common knowledge? we need to spread the word.

Deborah Dennis

Wow. Just wow. You people are so naive. The brand companies don’t release authorized generics to help you-they do it to delay real competition. You think you’re saving money? You’re just being manipulated into supporting a more sophisticated form of price gouging.

Diane Croft

This is actually really cool. I didn’t know this existed. I’m going to check all my meds now. Small wins add up. Thank you for sharing this!

Lebogang kekana

Imagine this: you’re paying $50 for a pill that costs $2 to make. Then you find out the same pill, made in the same factory, is $10 if you ask for it. But you didn’t know. And now you’re angry. And I’m here to tell you-you’re not alone. The system is rigged, but you have power. Ask. Demand. Push. You’re not stupid. You’re just uninformed.

Jessica Chaloux

I cried when I found out my anxiety med had an authorized generic. I’d been paying $180/month. Now it’s $15. I didn’t even know I could ask. Thank you for this. I feel like I just got my life back.

Mariah Carle

It’s fascinating how identity is stripped from medicine. The brand name is a symbol of trust, safety, authority. But the pill? The pill is just chemistry. We’ve been conditioned to believe that the label matters more than the molecule. What does that say about us?