Imagine walking into a pharmacy with a prescription for a brand-name medication. The pharmacist hands you the box, and the price tag is $150. But then they ask, "Do you want the generic version?" You nod, and suddenly that same treatment costs $4. This isn't just a lucky break; it's the result of a carefully engineered system called insurance benefit design, which uses strategic financial incentives to steer patients toward lower-cost medications. This system has become the backbone of modern healthcare cost containment. For decades, insurers and pharmacy benefit managers (PBMs) have relied on organizations that manage drug benefits for health plans by negotiating prices and creating formularies to push generic drug usage. Why? Because generics are significantly cheaper than their brand-name counterparts, often costing 80% to 85% less. In 2022 alone, generic drugs accounted for 91.5% of all prescriptions dispensed in the United States but only 22% of total drug spending. That’s a massive disparity that saves the healthcare system billions. But how exactly do these plans make this happen? It’s not magic-it’s math, policy, and a bit of behavioral psychology. Let’s look at the mechanics behind the scenes.

The Formulary Tier System: The Core Mechanism

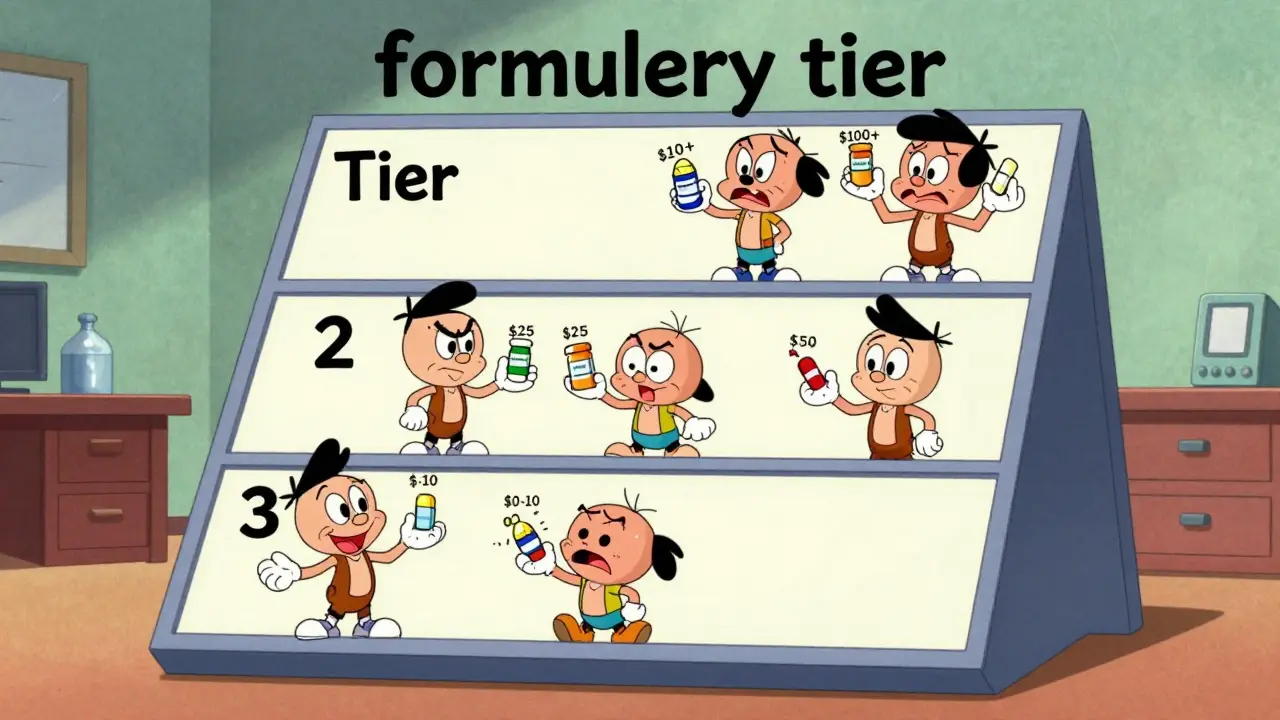

The most visible tool in insurance benefit design is the formulary, which is a list of covered medications organized by cost-sharing levels. Think of it as a menu where some dishes are cheap because they’re made with budget-friendly ingredients, while others are expensive luxury items. Most commercial health plans use a tiered structure:

- Tier 1: Preferred generic drugs. These usually have the lowest copayments, often ranging from $0 to $10 for a 30-day supply.

- Tier 2: Preferred brand-name drugs. If no generic exists or if your doctor insists on a specific brand, you pay more-typically $25 to $50.

- Tier 3: Non-preferred brands or specialty drugs. Here, costs can jump to $60, $100, or even higher, sometimes involving coinsurance where you pay a percentage of the total cost.

Mandatory Substitution and Step Therapy

Beyond just showing you different prices, many plans actively restrict access to brand-name drugs when a generic alternative exists. This is known as mandatory generic substitution, a practice allowed by law in all 50 states, enabling pharmacists to swap brand names for generics without prescriber approval. In 49 states, pharmacists can automatically substitute a generic for a brand-name prescription unless the doctor explicitly writes "Dispense as Written." This removes friction from the process. You don’t have to ask for the generic; it just happens. Another powerful tool is step therapy, also known as a protocol requiring patients to try lower-cost treatments before covering more expensive options. Imagine you need medication for high blood pressure. Your insurer might say, "Try the generic first. If it doesn’t work after three months, we’ll cover the brand-name drug." As of 2023, 92% of Medicare Part D plans used step therapy protocols. This ensures that patients exhaust cheaper options before moving up the cost ladder. These mechanisms aren’t just theoretical. A study published in *Health Affairs* found that a Medicare HMO using a generic-only benefit design saw a 15.2% reduction in overall prescription drug use and a 28.7% drop in brand-name medication utilization. That’s real money saved for both the insurer and the patient.

The Role of Pharmacy Benefit Managers (PBMs)

You can’t talk about insurance benefit design without mentioning PBMs. These middlemen sit between drug manufacturers, pharmacies, and health plans. Their job is to negotiate rebates and discounts. In 2022, PBMs processed 6.8 billion generic prescription claims and secured an estimated $195 billion in rebates for health plans, according to the Pharmaceutical Care Management Association (PCMA). However, this relationship is complex-and controversial. While PBMs claim they drive affordability, critics argue that opaque pricing practices prevent patients from seeing the full benefit of generic savings. A 2022 white paper from the USC Schaeffer Center highlighted that patients might overpay by $10 to $15 per generic prescription due to spread pricing-a practice where PBMs charge health plans more than they reimburse pharmacies, keeping the difference. So, while the system is designed to cut costs, the distribution of those savings isn’t always transparent. Some of the money saved goes back to the insurer or PBM, rather than directly to your pocket. This is why understanding your plan’s specifics matters more than ever.

Comparing Insurance Programs: Medicare, Medicaid, and Commercial Plans

Not all insurance programs handle generics the same way. Let’s break down how three major systems approach cost control:

| Insurance Type | Generic Copay Range (2024) | Key Cost Control Mechanism | Generic Dispensing Rate |

|---|---|---|---|

| Medicare Part D | $0 - $15 | Standardized tiered formularies; mandatory generic tiers | High (varies by plan) |

| Medicaid | Low fixed copays or $0 | Federal Upper Payment Limits (UPL); reference-based pricing | 89.3% (2022) |

| Commercial Plans | $0 - $10 (Tier 1) | HDHPs with HSAs; high-deductible structures | 87.1% (2022) |

Real-World Impact: Savings and Patient Experiences

Does this system actually work? The numbers say yes. From 2013 to 2022, generic drugs saved the U.S. healthcare system approximately $3.7 trillion, according to the IQVIA Institute. That’s $370 billion in annual savings. For self-insured employers, the impact is tangible. A Johns Hopkins University study found that two large companies substituting therapeutically equivalent lower-cost options achieved savings between 9% and 15% without harming patient outcomes. But what about the people taking the pills? Patient experiences are mixed. On one hand, satisfaction is high. A January 2024 survey by the Kaiser Family Foundation found that 68% of Medicare Part D beneficiaries were satisfied with their generic drug coverage, compared to just 42% for brand-name drugs. Many appreciate the predictability of low copays. On the other hand, frustration exists. Some patients report issues with prior authorization when doctors insist on brand-name drugs. Others encounter unexpected costs due to copay clawbacks or formulary restrictions. In a 2023 Medscape poll, 31% of physicians reported patients experiencing adverse effects after being switched to generics through insurance-mandated substitutions. While rare, these cases highlight that clinical equivalence doesn’t always mean identical tolerability for every individual. Additionally, alternative models are emerging. The Mark Cuban Cost Plus Drug Company, launched in 2022, offers transparent pricing for 124 generic drugs. An economic evaluation found patients could save a median of $4.96 per prescription by buying directly, particularly benefiting uninsured individuals. This challenges traditional PBM models and pushes for greater transparency.

Future Trends: Transparency and Regulation

The landscape of insurance benefit design is evolving. One major shift is increased transparency. Starting January 1, 2025, the Department of Labor mandated enhanced disclosure in Explanation of Benefits (EOB) statements. Patients will now see detailed breakdowns of generic drug pricing components, helping them understand why they’re paying what they’re paying. Regulatory changes are also underway. The Inflation Reduction Act allows Medicare to negotiate drug prices, with the first negotiated prices available in 2026 for Part D drugs. The Congressional Budget Office estimates this will generate $98.5 billion in savings over ten years. Meanwhile, CMS is launching the GENEROUS Model in 2026, aiming to reduce Medicaid drug spending by $40 billion over a decade through centralized negotiation. For consumers, the key takeaway is this: insurance benefit design is a powerful tool for cutting costs, but it requires vigilance. Understand your formulary tiers, ask your pharmacist about generic alternatives, and check if your plan uses step therapy. By working within the system, you can maximize your savings while staying healthy.

What is insurance benefit design?

Insurance benefit design refers to the strategic structuring of health plan features, such as copayments, deductibles, and formularies, to influence patient behavior and control costs. In the context of prescriptions, it often involves incentivizing the use of generic drugs through lower out-of-pocket expenses.

Why do insurance plans prefer generic drugs?

Generic drugs typically cost 80-85% less than brand-name equivalents. By steering patients toward generics, insurers and employers can significantly reduce prescription drug spending. In 2022, generics represented 91.5% of prescriptions but only 22% of total drug spending, highlighting their efficiency in cost containment.

How do formulary tiers affect my medication costs?

Formularies categorize drugs into tiers based on cost. Tier 1 usually includes preferred generics with the lowest copays ($0-$10). Tier 2 and 3 include brand-name and specialty drugs with higher copays ($25-$100+). Choosing a Tier 1 generic can save you dozens of dollars per prescription compared to a brand-name alternative.

Can I refuse a generic substitution?

Yes, but it may cost you more. In most states, pharmacists can automatically substitute generics unless your doctor specifies "Dispense as Written." If you prefer the brand-name drug, you’ll likely face a higher copayment or coinsurance, depending on your plan’s formulary tier structure.

What is step therapy in insurance plans?

Step therapy is a protocol where insurers require patients to try lower-cost medications (usually generics) before approving coverage for more expensive brand-name drugs. If the initial treatment fails, your doctor can appeal to get the brand-name drug covered. This is common in Medicare Part D and commercial plans.

Are generic drugs as effective as brand-name drugs?

Yes. The FDA requires generic drugs to be bioequivalent to their brand-name counterparts, meaning they contain the same active ingredient, strength, and dosage form. While inactive ingredients may differ, clinical outcomes are generally identical. However, a small percentage of patients may experience sensitivity to specific fillers or binders.

How do PBMs influence generic drug pricing?

Pharmacy Benefit Managers (PBMs) negotiate rebates and discounts with drug manufacturers. They create formularies that prioritize generics to control costs. While they secure billions in savings for health plans, critics argue that opaque practices like spread pricing may prevent patients from realizing the full extent of these savings.

What changes are coming for Medicare drug costs in 2025-2026?

Starting in 2025, Medicare Part D beneficiaries have an annual out-of-pocket cap of $2,000. Additionally, the Inflation Reduction Act allows Medicare to negotiate drug prices, with the first negotiated prices for select drugs becoming available in 2026. These changes aim to further reduce costs for seniors.